Gonzales Mayor Barney Arceneaux

Rarely have Ascension’s three municipalities united against a common threat, real or perceived. Thursday was one of those occasions when two east bank mayors crossed the Sunshine Bridge to join Donaldsonville’s Leroy Sullivan. They oppose an ordinance proposed by Parish President Clint Cointment seeking a larger share of sales tax generated on properties annexed by one of them, the ordinance tabled by a skeptical Parish Council promising to meet with the mayors prior to taking it back up.

Sorrento’s Mayor Chris Guidry, and Gonzales Barney Arceneaux (with the city council along), joined Mayor Sullivan in opposition.

President Cointment lobbied to have the item removed from last night’s agenda, preferring time to clear up “a lot of misinformation about this whole process.” Chairman Chase Melancon rejected his overtures, citing Ascension’s Home Rule Charter which, arguably, requires a public hearing once any ordinance has been introduced. The January 18 agenda included:

Introduction of Ordinance – to amend ordinance Sec.9-5 Sharing of sales tax revenue between the parish and municipalities generated by annexed properties from 50/50 split with the Parish and the City of Gonzales to a 75(Parish)/25 (City) split.

Singling out “the City of Gonzales” when the subject ordinance applies to annexations by the City of Donaldsonville and the Town of Sorrento attracted the former’s attention and Gonzales CAO Scot Byrd lobbied against introduction.

https://pelicanpostonline.com/rift-brewing-between-parish-and-city-of-gonzales-over-tax-sharing-ordinance/

to no avail. Whoever was responsible, and no one is fessing up, it was a faux pas compounded by the fact that nary a council member knew much of anything at all about the initiative either.

The only council member to utter a word on on January 18 was Joel Robert whose reconfigured District 2 includes the City of Gonzales’ southeasternmost quadrant. In reply, President Cointment assured that an actual information packet would be made available to the council prior to its vote. 12 days later…and council members had yet to receive any of the promised information.

What was finally provided on Tuesday…

and an Excel spread sheet that may as well have been written in Mandarin Chinese for its complexity (or maybe it was pure gibberish), made things worse.

President Cointment sought a delay until the March 2 council meeting date in order to “get a packet together for the municipalities.” Which begs the question why three municipalities were not informed prior to the ordinance’s introduction, not to mention 11 ignorant members of the governing authority who spent two weeks fielding phone calls from angry mayors and municipal council members, unable to explain why the ordinance needs to be amended.

“Because we have unfunded mandates, because we’re trying to grow responsibly with balanced infrastructure,” President Cointment explained last night. “That’s the reason we want to go back to the 75/25 (split).”

Ascension Parish must proving funding for several entities out of its General Fund, with no dedicated funding.

- 23rd Judicial District Court

- 23rd JDC District Attorney

- Coroner’s Office

- Justices of the Peace/Constables

- Registrar of Voters

- Juvenile Services

- Office of Emergency Preparedness

- Economic Development

“Every parish citizen, including those in municipalities, gets the benefits,” Cointment argued, going on to claim that funding demand for the enumerated services will “increase by $4 million from last year.”

A reasonable argument that might be compelling once broken down in a user friendly format.

There was a second justification. Cointment, pointing at Conway Subdivision, asserted that Ascension Parish development requirements are stricter than the city’s.

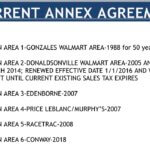

By Inter-Governmental Agreement dated July 3, 2018 four taxing authorities (City of Gonzales, AP Law Enforcement District, AP Rural Sales Tax District and AP Sales Tax District No. 2) executed the tax sharing agreement for Conway. Each accepted half of the total sales tax available to it on “approximately 400 acres” acquired by Southern Lifestyle Development, LLC from the MP Evans Estate, annexed by Gonzales in February of 2012.

Conway Subdivision master plan

Total Tax available/(Adjusted Rate pursuant to agreement):

- City of Gonzales – 2% (1%)

- Rural Tax District – 1% (.5%)

- Sales Tax District No. 2 – .5% (.25%)

- Law Enforcement District – .5% (.25%)

The rationale; that effected entities are subject to the same total 2% sales tax as everyone else, either inside the City of Gonzales or the unincorporated Ascension Parish. The argument can be (in fact, has been) made by the city that no sales tax is being generated on the undeveloped tracts it annexes, and businesses seek annexation to enjoy services provided by Gonzales unavailable outside its city limits. Most prominently, Gonzales provides water and wastewater treatment, emergency medical services and twice weekly garbage collection with recycling unlike Ascension Parish.

Gonzales also picks up the tab for law enforcement and fire protection in newly annexed properties, lessening the burden on APSO and various fire districts.

“All we ever wanted was a conversation to occur regarding any changes to this specific ordinance,” insisted City Attorney Matthew Percy who proceeded to make Gonzales’ case.

City Attorney Matthew Percy

Considering all those services in Gonzales, “there is no basis for a 75/25 split” in favor of Ascension. Percy lobbied for an examination of the respective costs borne by the city versus Ascension’s “unfunded mandates.” Mayor Arceneaux echoed those sentiments, lamenting Gonzales’ exclusion from the process.

“We’re not asking to do anything new,” President Cointment pointed out that the original ordinance codified the 75/25 equation in the parish’s favor, assuring that “no existing agreements will be affected.”

Whatever is being requested, it will await another day. The agenda item was “tabled” without setting a date for council consideration. but with the understanding that three municipalities will have the opportunity to weigh in.

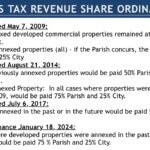

Section 9-5 was enacted by the Parish Council on May 7, 2009, then called Sales Tax Enhancement Plan. It read:

Previously Annexed Property: In all cases where developed commercial properties were annexed prior to the effective date of this Sales Tax Enhancement Plan, fifty percent of the net proceeds shall be retained by the Districts and fifty percent of the net proceeds shall be paid to the municipality. The net sales tax revenues shall be those received by the District after accounting for all expenses of collection.

Subsequently Annexed Property: In all cases where properties are proposed to be annexed following the effective date of this agreement, unless the Parish Council concurs in the annexation, within the allowable days, the entire net proceeds shall be retained by the Districts. In all cases where properties are proposed to be annexed following the effective date of this agreement, the Parish Council shall not arbitrarily refuse to concur in the annexation. For purposes of this Plan, arbitrary refusal to concur means the absence of a compelling interest, either in terms of the loss of a significant tax revenue or the potential for adverse impacts to life, property or the general welfare of the residents of Ascension Parish. In those cases where the Parish concurs in the annexation, the Districts shall retain seventy five percent of the net proceeds and twenty five percent of the net proceeds shall be paid to the municipality.

Future Taxes Not Affected: This Plan is intended to apply only to existing sales taxes. Additional sales taxes which may be levied in the future by any entity with such authority shall be entirely payable to the levying.

On August 21, 2014 it was revised to read:

Previously Annexed Property: In all cases where properties were annexed prior to the effective date of the Original Sales Tax Enhancement Plan, May 7, 2009, fifty percent of the net proceeds shall be retained by the Districts.

Subsequently Annexed Property: In all cases where properties are proposed to be were or are annexed after May 7, 2009, the Districts shall retain seventy-five percent of its sales

taxes.Future Taxes Not Affected: Any additional sales taxes shall not be affected by this Ordinance.

The Ordinance regulates the percentage of sales taxes to be received by Ascension Parish Sales Tax District #1 and Ascension Parish Sales Tax District #2, any municipality impacted by this Ordinance may retain any portion of the sales taxes for which it is legally authorized to receive and/or collect.

And again on July 6, 2017:

The sales tax enhancement plan attached hereto and made a part hereof as Exhibit A be implemented and that the office of the parish president is hereby authorized to enter into such

agreements as contemplated by this plan.(1) In all cases where developed properties were annexed in the past or are annexed in the future, fifty (50) percent of the net proceeds shall be collected and retained by the districts. The net sales tax revenues shall be those received by the District after accounting for all expenses of collection.

(2) Future taxes not affected: This plan is intended to apply only to existing sales taxes. Additional sales taxes, which may be levied in the future by any entity with such authority, shall be entirely payable to the levying authority, unless provided for in any sales tax enhancement plan entered into between the districts and municipality.

PROPOSED ORDINANCE (would only change Paragraph 1 immediately above):

(1) In all cases where developed properties were annexed in the past or are annexed in the future, eventy-five (75) percent of the net proceeds shall be collected and

distributed to the Parish and twenty-five (25) percent of the net proceeds shall be collected and retained by the districts. The net sales tax revenues shall be those received

by the district after accounting for all expenses of collection.